Deleveraged Bitcoin, the Next Winner of Global Capital Flows

Original Title: Bitcoin - the trade after the trade

Original Author: fejau

Original Translation: Deep Tide TechFlow

I would like to write about a question that I have been contemplating for a while: how might Bitcoin behave in a scenario of significant capital flow transformation, a situation that Bitcoin has never experienced since its inception.

I believe that once deleveraging is completed, Bitcoin will see an incredible trading opportunity. In this article, I will elaborate on my thought process.

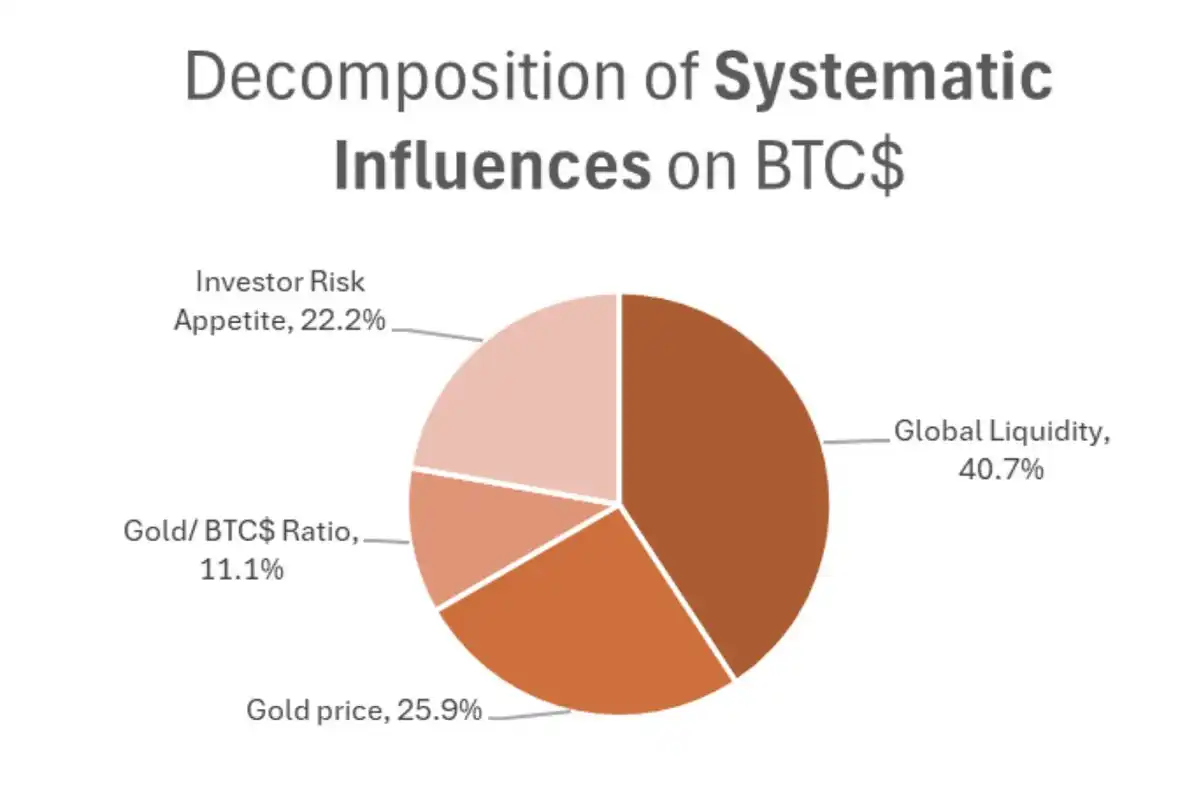

What are the Key Historical Drivers of Bitcoin's Price?

I will adopt Michael Howell's research on the historical drivers of Bitcoin's price and use these findings to further understand how these interrelated factors may evolve in the near future.

As shown in the chart above, Bitcoin's driving factors include:

· Overall demand for high-risk, high-β assets by investors

· Correlation with gold

· Global liquidity

Since 2021, I have used a simple framework to understand risk appetite, gold performance, and global liquidity, focusing on the percentage of fiscal deficit to GDP as a convenient way to grasp the fiscal stimulus dominating global markets since 2021.

A higher percentage of fiscal deficit to GDP mechanically leads to higher inflation, higher nominal GDP, and thus higher total corporate revenue since revenue is a nominal metric. This is a boon for companies that benefit from economies of scale in their profit growth.

In most cases, monetary policy plays a secondary role in risk asset activity, with fiscal stimulus being the primary driver. As shown in this chart regularly updated by @BickerinBrattle, the U.S. monetary stimulus is so tepid compared to fiscal stimulus that I will set it aside in this discussion.

As shown in the chart below, among the major developed Western economies, the U.S. fiscal deficit as a percentage of GDP is much higher than any other country.

Due to the large deficit in the United States, income growth has always been predominant, leading to the strong performance of the US stock market compared to other modern economies:

Due to this dynamic, the US stock market has become the main marginal driver of asset growth, wealth effect, and global liquidity, making it an attractive destination for global capital: the United States. With this dynamic of capital inflows into the US, coupled with a massive trade deficit, the US exchanges goods for US dollars obtained from foreign sources, which are then reinvested in US dollar-denominated assets (such as Treasury bonds and MAG7). The United States has become a major driver of global risk appetite.

Now, back to the aforementioned research by Michael Howell. Risk appetite and global liquidity have been mainly driven by the United States over the past decade, and this trend has accelerated since the onset of the COVID-19 pandemic due to the US's significant fiscal deficit compared to other countries.

Therefore, Bitcoin, although a global liquidity asset (not just in the US), has shown an increasing positive correlation with the US stock market since 2021.

Now, I believe that the correlation with the US stock market is misleading. When I use the term "spurious correlation" here, I am, from a statistical perspective, suggesting that there is a third unobserved variable in the correlation analysis that is the actual driving factor. I believe this factor is global liquidity, as mentioned earlier, which has been predominantly led by the US over the past decade.

As we delve into discussions of statistical significance, we must also establish causality, not just correlation. Fortunately, Michael Howell has also done some excellent work in this regard, establishing a causal relationship between global liquidity and Bitcoin through Granger causality testing.

So, what does this provide us as a starting point?

Bitcoin is primarily driven by global liquidity, and as the United States is a key driver of global liquidity expansion, a spurious correlation has emerged.

Over the past month, as we speculate on Trump's trade policy objectives and the reshuffling of global capital and commodity flows, some key narratives have emerged. I see it as:

The Trump administration aims to reduce the trade deficit with other countries, which mechanically means reducing the outflow of US dollars to foreign countries, dollars that will not be reinvested in US assets. The reduction in the trade deficit cannot occur without this happening.

The Trump administration believes that foreign currencies are artificially suppressed, causing the US dollar to be artificially strong, and aims to rebalance this. In short, a weaker dollar and stronger foreign currencies will lead to higher rates in other countries, prompting capital inflows to capture these improved post-forex-adjustment conditions rates as well as domestic equities.

Trump has taken a "shoot first, ask questions later" approach in trade negotiations, leading other countries around the world to move away from slim fiscal deficits compared to the US (as described above) and instead invest in defense, infrastructure, and broadly protectionist government investments to make themselves more self-reliant. Regardless of whether tariff negotiations are downgraded (e.g., China), I believe this is now a fait accompli, and countries will continue to pursue this goal.

Trump wants other countries to increase their defense spending as a percentage of GDP and contribute more to NATO spending as the US bears a significant amount of the expense. This will also increase the fiscal deficit.

I will temporarily set aside my personal opinions on these points and focus on the potential impact if we were to drive towards the logical conclusion of these narratives:

Capital will leave dollar-denominated assets and flow back to the home country. This means that the US stock market will underperform relative to the rest of the world, bond yields will rise, and the dollar will weaken.

This capital will flow back to areas where fiscal deficits are no longer constrained, and other modern economies will start spending and printing money on a grand scale to fund these increased deficits.

As the US shifts from a global capital partner to a more protectionist role, holders of dollar assets will have to increase the risk premium on these once pristine assets and mark them to a wider safety margin. As this process unfolds, it will lead to rising bond yields, foreign central banks will seek to diversify their balance sheets away from just US treasuries to other neutral assets like gold. Similarly, foreign sovereign wealth funds and pension funds may also pursue such diversification.

The flip side of these views is that the US is the center of innovation and technology-driven growth, and no country will overturn that idea. Europe is too bureaucratic and socialized to pursue capitalism like the US. I sympathize with this view; it may mean this is not a multi-year trend but a mid-term trend, as the valuations of these tech companies will cap their upside for a while.

Returning to the title of this article, the first trade is to sell the world drastically over-allocated in dollar assets to avoid the ongoing deleveraging. As the world holds too many of these assets, when risk limits are hit by large money managers and more speculative players such as tight-stop multi-strategy hedge funds, this deleveraging can become messy. When this happens, we will see days akin to margin calls, where all assets need to be sold to raise cash. The strategy now is to survive and maintain ample liquidity.

However, as the deleveraging subsides, the next phase of trading begins—transitioning to a more diversified investment portfolio: foreign equities, foreign bonds, gold, commodities, and even Bitcoin.

On market rotation days and non-margin call days, we have already started to see this dynamic take shape. The US Dollar Index (DXY) is declining, the US stock market is underperforming compared to other regions' stock markets, gold is surging, and Bitcoin is surprisingly holding up well compared to traditional US tech stocks.

I believe that as this situation unfolds, the marginal increase in global liquidity will shift towards the exact opposite dynamic we are used to. Other regions will take on the responsibility of increasing global liquidity and risk appetite.

When contemplating the risks of this diversification against the backdrop of a global trade war, I am concerned about the tail risks of delving too deeply into other countries' risk assets, as there are some major landmines in terms of potentially bad tariff news. Therefore, this makes gold and Bitcoin choices for globally diversified investments in this transition.

Gold has been on an absolute tear, hitting new all-time highs daily, reflecting this regime change. However, while Bitcoin has surprisingly held up well throughout the entire regime change process, its beta correlation to risk appetite has so far limited its performance, failing to keep up with gold's performance.

Thus, as we move towards a rebalancing of global capital, I believe the next trade after this is Bitcoin.

As I contrast this framework with Howell's relevance research, I can see them coming together:

The US stock market cannot escape the influence of global liquidity, only being measured by liquidity from fiscal stimulus plus some inflows (but we have just identified that this aspect of flow may stop or even reverse). However, Bitcoin is a global asset, reflecting this broad perspective of global liquidity.

With the establishment of this narrative and allocators continuing to rebalance, I believe risk appetite will be driven by regions other than the US.

Gold has performed exceptionally well, so for the Bitcoin portion associated with gold, we can also check the box here.

Given all this, for the first time in the financial markets, I see the potential for Bitcoin to decouple from US tech stocks. I know this idea often marks a local top for Bitcoin. What's different this time is that we see the potential for a significant shift in capital flows, which will make it enduring.

Therefore, for someone like me, a risk-loving macro trader, Bitcoin feels like the purest trade here. You can't levy tariffs on Bitcoin, it doesn't care where it resides geographically, it provides a high beta to the portfolio without the current tail risks associated with US tech, I don't have to opine on whether Europe can get its act together, and it offers a pure exposure to global liquidity, not just US liquidity.

This market structure is exactly the reason Bitcoin was born. Once the dust of deleveraging settles, it will be the fastest horse, accelerating forward.

You may also like

How to choose between buying discounted ETH, Bitmine, and SharpLink?

Semiconductor stocks plummet, yet Anthropic wants to create a 2nm chip

A South Korean company that learned the strategy of hoarding coins, from a bull market to delisting?

Where is Zhao Changpeng's billion-dollar investment going? YZi Labs' investment landscape fully revealed

Ethereum Foundation Report: A Basic Guide to Ethereum for Governments and Financial Institutions

A pre-announced harvesting case: After the cryptocurrency price dropped by 99%, the public chain Saga exited to transform into AI

When American giants collectively "defect" from Chinese AI models

BIS Report Compliance Observation: The Real Risks of Stablecoins, Not Just "Depegging"

Portugal 2-1 Croatia: Ronaldo's 20-Year Knockout-Stage Drought Ends With a Debt Finally Collected

Portugal beat Croatia 2-1 in the 2026 global football championship's knockout rounds as Ronaldo scored his first-ever knockout-stage goal, Gonçalo Ramos struck a stoppage-time winner, and VAR ruled out a late equalizer for offside.

Bitcoin Price Prediction July 2026: Will BTC Recover to $70K or Drop Below $55K?

WEEX API Broker Program: Turn Your Trading Platform Into a Revenue Engine

Do you want to buy CRCL?

Wosh: Inflation has cooled in recent weeks, AI is reshaping the economy, and forward guidance has lost its necessity

The most secretive AI winner

Looking at Stripe's ambitions and the future of stablecoins from OUSD

From Pump.fun to Collector Crypt: Has Solana's income throne changed hands?

Dan Bin's latest speech: Don't miss out on a great era